Happy New Year! We are continuing the initiative started last year. Each week The Glenn Team provide highlights from the weekly CP office meeting to provide a balanced overview of the Toronto and GTA markets and relevant issues affecting real estate markets. Meetings are overseen by Chestnut Park's CEO and Broker of Record, Chris Kapches, LLB, who provides weekly analysis and commentary. Additional input is provided by the CP Toronto office Realtors who give a day to day, real life perspective of the local markets.

As we move into 2018, we've been a bit slow on the uptake given the seemingly relentless strain of viruses going around. Whether it's the result of extreme cold or too many holiday revelries, we encourage everyone to stay warm and healthy this new year! Now onto the meeting...

REWIND & FAST FORWARD - 2017 into 2018

To begin this recap, we have a recap! Chris thought it best to review some of what affected 2017's market as we go into 2018. Canada was the top performing country in the G7 with an annual growth rate of 3%. Consumer activity drove the majority of growth throughout the year; though is expected to slow in 2018. Economists are estimating anywhere b/w 2-5%, with 2% being the more realistic expectation. Unemployment is now below 6% nationally having created around 79,000 jobs, but Canada is still behind the U.S. (4.1%), Japan (2.8%), Germany (3.6%) and the U.K. (4.2%); there is anticipation those unemployment numbers will continue to drop. The downside there is that lower unemployment will lead to hikes in Interest rates. Canada is currently the most indebted nation in the world, with 170% debt to household income, so some adjustment to prices in the housing market would be helpful to most.

There is another rate hike by the Bank of Canada anticipated and the new stress test has officially been implemented. Given both of those factors, some economists speculate about 10% of the buyers in Toronto to drop out of the market. Chris doesn't share this sentiment given many buyers have had to qualify at the stress test rates prior to January 1st. The new stress test is unlikely to impact housing volume but likely will impact sale prices. If a buyer with 20% down was approved at $800K in 2017, the same buyer today may only be able to get $650K. Buyers may start offering less for less or seller’s may find they need to lower their price point, but anyone purchasing properties over $1.5M are unlikely to be affected given the downpayment required for such properties. What IS likely to be affected is the condo market, as condos remain the most affordable property on the market, regardless of lack of inventory.

Uncertainties that for 2018 include NAFTA talks and the upcoming election in Ontario. Both will play key roles in shaping the economy and subsequently, our housing market. Overall, however Chris felt that there was nothing seriously bad on the horizon for the housing market this year but given it is a year of uncertainty in certain areas and that last year saw what he called “most incredible oscillation in real estate” and a “very, very tumultuous year”, we should expect to see decent sales and more normalized sale price increases.

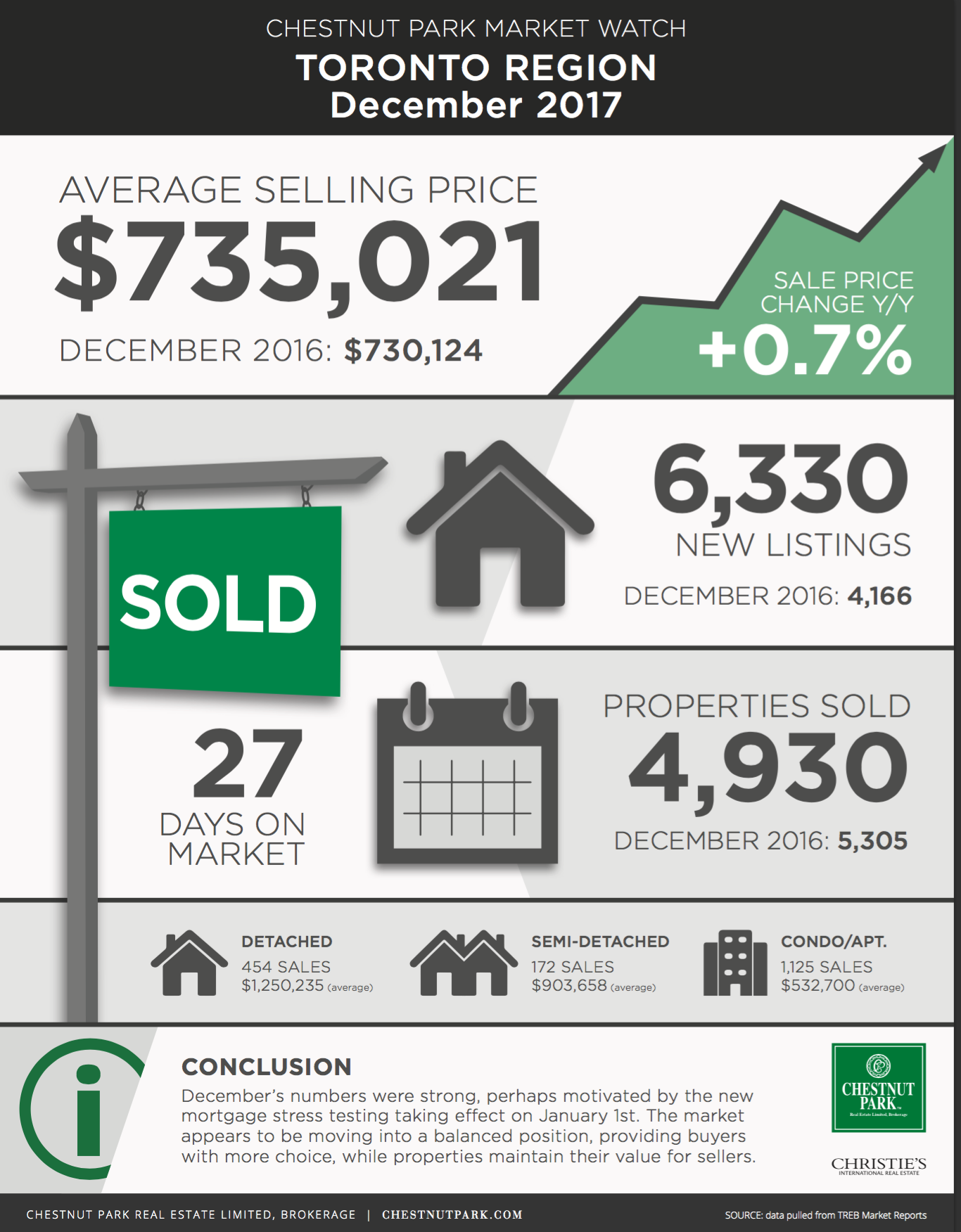

DECEMBER MARKET STATS

December is typically a "boring" month stats-wise as the market tends to die down with people getting into holidays. What we do get however are the stats for the year. This year saw a high total for number of sales reaching coming in just over 92,000 for the GTA, about 2% below 2016's highs of 113,000; the most sales ever seen in TREB's history. The bulk of those sales took place prior to May, after which, the drastic drop in activity and prices took place. Our total for 2017 ranks in the top 4 number of sales over the course of the TREB. For December, the average sale price came in at $735,000 across the GTA ($741,000 in the 416), with 4930 sales total. That's an increase in both the average sale price and sales volume year/year. The average sale price for detached properties in the 416 was $1,250,000 (-2.8% yr/yr). In the 905, the average was $910,000, further echoing the disparity b/w both markets. Semi-detached properties averaged $903,000 (+11.5% yr/yr) and condominiums came in at $532,000 (+14.1% yr/yr) in the 416. Given these numbers, clearly buyers are still unwilling to pay the high prices some sellers still demand for detached properties and are moving to more affordable property types; a trend no doubt to continue into 2018. All properties sold in 27 days or less, which remains a fast market pace.

The number of high-end properties (over $2M+) for the month came in at 116, including 7 condominium apartments, so some condos are now inching up to that $2M+ range as well. Toronto's East end seems to remain the strongest area for price and time to sale, with all properties being sold for 100% of asking or more. Other areas of the city are not going for 100% of ask so it’s likely sellers will be pricing properties to sell as opposed to expecting a flood of buyers to pay the big prices we saw at the beginning of 2017. Overall, the data for December is very positive. There is a strong likelihood that the media will report huge drops in prices when January’s numbers come out and may paint a negative picture of the market but that’s only due the the over-inflated prices from the early part of 2017.

Here's a handy infographic developed by Chestnut Park's marketing team giving a summary of the December stats.

PERIODIC PIECE

Changes to the Condominium Act in the late part of 2017 introduced the requirement of condominium boards producing a Periodic Information Certificate. This PIC is much like the summary retained in most Status Certificates without the attachments. It provides general information on the property, who the property management for the building is, the number of units leased in the building, directors of the corporation and addresses to contact them. It also gives details regarding insurance amounts for the building along with deductibles and financial Information to get some stance of the financial stability of the corporation, ie. the amount of expenses, liabilities and any foreseen costs coming up, or what the increase to the reserve fund will be going forward. Lastly, it details any legal action or party to judgements the corporation has. This document should be issued every 6 months to condo owners, so if you live in a condominium currently and have yet to receive one, you should contact your property manager to inquire. This is a helpful document for anyone thinking about selling their unit or simply interested in how their building is doing in a general sense.

Are you finding these meeting recaps useful? We'd love to hear from you! Feel free to leave a comment below or get in touch directly!